You opened your account. You made your first investment. Maybe you bought one index fund, set up an automatic transfer, and told yourself you’d figure out the rest later.

Later is now.

You’re looking at that single fund and wondering: is this actually a portfolio? Should there be more? What about bonds? International stocks? And what does “rebalancing” even mean? Is that something you’re supposed to be doing?

This guide picks up exactly where the basics leave off. You’ll learn what a real investment portfolio looks like, how to choose an asset allocation that fits your timeline, and how to keep everything on track without turning it into a part-time job. Three model portfolios are laid out below, ready to use today, no finance degree required.

What you’ll learn:

- What a portfolio actually is (and why one fund is a legitimate starting point)

- The one concept that drives every portfolio decision: asset allocation

- Three model portfolios, from simplest to slightly more structured

- A step-by-step process to build and maintain your portfolio

- How to rebalance without overcomplicating it

- How your portfolio connects to your FIRE number and timeline

If you haven’t started investing yet, begin here first:

How to Start Investing for Beginners: A Simple Guide to Your First Investment

What a Portfolio Actually Is (and Why One Fund Can Be Enough)

A portfolio is simply the full collection of your investments: every account, every fund, every asset, looked at together as a whole. That’s it. There’s no minimum number of funds required and no complexity threshold you have to cross before it “counts.”

For many beginners, a single broad-market index fund genuinely is a complete portfolio. It already holds thousands of companies across different sectors and sizes. It’s diversified, low-cost, and requires almost no maintenance. If that’s where you are right now, you’re not doing it wrong.

So why think about building something more intentional? Two reasons.

First, as your portfolio grows, the absolute dollar amounts at stake get larger. A 30% market drop on a $5,000 portfolio is uncomfortable but survivable. The same drop on a $300,000 portfolio is a different psychological experience entirely. Understanding your allocation helps you build a portfolio you can stay in through turbulent markets. That is the whole game.

Second, your FIRE timeline shapes your portfolio. Someone with 25 years to invest can absorb more short-term volatility than someone three years from their target. Thinking intentionally about structure means your portfolio evolves with your plan, not against it.

For a refresher on the building blocks (index funds, compound growth, account types), the investing primer covers all of it: How to Start Investing for Beginners.

The One Concept That Drives Every Portfolio Decision: Asset Allocation

Asset allocation is how you divide your money between different types of investments, primarily stocks and bonds. Everything else in portfolio design flows from this one decision.

Here’s why it matters: different asset classes behave differently in different market conditions. Stocks tend to deliver stronger long-term growth, but they also drop sharply during downturns. Bonds tend to hold their value better during stock market crashes, but they grow more slowly over time. The mix you choose determines both your expected return and how much turbulence you’ll experience along the way.

The key insight: asset allocation isn’t about chasing the highest possible return. It’s about matching your portfolio to your timeline and your real ability to stay the course when markets fall. A portfolio you’ll panic-sell during a downturn is worse than a slightly more conservative portfolio you’ll hold through it.

The Simple Rule Most FIRE Investors Use

A common starting point is a rule of thumb: subtract your age from 110. The result is roughly your stock percentage. A 35-year-old would land at 75% stocks, 25% bonds. A 45-year-old at 65% stocks, 35% bonds.

This is a starting point, not a rule. Many FIRE investors run more aggressive allocations (80% to 100% stocks) because their investment horizons are long and they understand that short-term drops are temporary. Others prefer a more balanced mix because it lets them sleep through market downturns without second-guessing their plan. Neither is wrong. The right allocation is the one you’ll actually hold.

One place where allocation matters more than most beginners realise: Coast FIRE. The whole strategy depends on investing aggressively early, then leaving the portfolio alone for decades. That only works if your allocation can survive the volatility of those early years without you panic-selling.

What About International Stocks?

A third ingredient you’ll often see in FIRE portfolios is international stocks: funds that own companies outside the US. The argument for including them: diversification across different economies, currencies, and market cycles. When US markets underperform, international markets sometimes offset that. History shows periods where each has led the other.

The argument against: a total US market fund already includes companies earning the majority of their revenue globally. Apple, Amazon, and Coca-Cola aren’t purely domestic businesses. Some investors consider this sufficient international exposure without holding a separate fund.

Both positions are defensible. Whether you include international stocks is a choice, not a requirement. The model portfolios below show you what both approaches look like in practice.

Three Simple Portfolio Models

The three portfolios below cover the range from absolute simplicity to a slightly more structured setup. All three use low-cost index funds or ETFs. All three are widely used in the FIRE community. Pick the one that fits your current situation and preference. You can always adjust later.

The One-Fund Portfolio (Maximum Simplicity)

A single total-world index fund owns everything in one package: US stocks, international stocks, and sometimes a small allocation to bonds, all automatically maintained by the fund itself. You buy one fund and you’re done.

Best for: complete beginners, anyone who wants zero ongoing decisions, smaller portfolios where simplicity is the priority.

What to look for: a “total world” or “global market” index fund or ETF with a low expense ratio (under 0.20%, ideally under 0.10%).

The tradeoff: you accept whatever allocation the fund manager maintains. You can’t dial up or down the stock/bond ratio yourself. For most beginners, that is fine. The default allocation is usually growth-oriented and reasonable.

Maintenance required: almost none. Review once per year to confirm your automatic contributions are still running.

The Two-Fund Portfolio (One Step Up)

Two funds: a broad stock market index and a broad bond market index. You control the split.

Best for: investors who want to set their own stock/bond ratio but keep the portfolio simple. One step up from a single fund, without adding meaningful complexity.

Example allocation (aggressive, long timeline): 90% stocks / 10% bonds

Example allocation (moderate, medium timeline): 70% stocks / 30% bonds

Here’s what an 80/20 split looks like on a $10,000 portfolio:

| Fund | Allocation | Dollar Amount |

|---|---|---|

| Total stock market index | 80% | $8,000 |

| Total bond market index | 20% | $2,000 |

| Total | 100% | $10,000 |

Maintenance required: rebalance once per year if the allocation drifts significantly from your target.

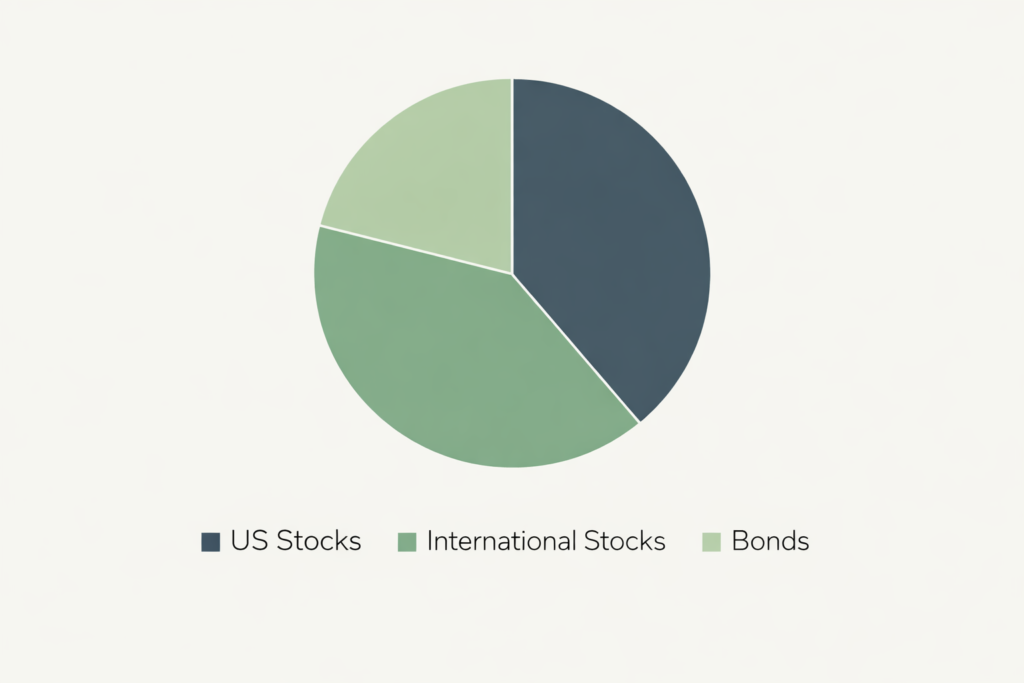

The Three-Fund Portfolio (The FIRE Community Standard)

Three funds: US stocks, international stocks, and bonds. This is the portfolio structure most commonly recommended in the Bogleheads community and across FIRE forums, and for good reason. It gives you broad diversification across the global economy while keeping the number of moving parts to a minimum.

Best for: investors who want explicit international exposure and a bit more control over each slice of their portfolio.

Example allocation (moderate FIRE, 12–15 year timeline):

| Fund | Allocation |

|---|---|

| US total stock market index | 60% |

| International stock market index | 20% |

| Total bond market index | 20% |

Example allocation (aggressive FIRE, 20+ year timeline):

| Fund | Allocation |

|---|---|

| US total stock market index | 70% |

| International stock market index | 20% |

| Total bond market index | 10% |

As you get closer to your FIRE date, you would typically shift the bond allocation higher, reducing exposure to stock market volatility at the point when you’re about to start drawing from the portfolio.

Maintenance required: rebalance once per year. With three funds, this takes around 20 minutes.

Two books that go deep on this approach and are worth reading once you’ve got your first portfolio running: The Bogleheads’ Guide to Investing and Just Keep Buying, which makes a rigorous, evidence-based case for consistent investing and ignoring short-term noise.

Worked Example: What These Portfolios Look Like in Practice

Two people, same starting point, different choices based on their situations.

Alex, 32, aggressive FIRE timeline: Alex earns $5,000/month after tax, invests $600/month, and is targeting FIRE at 47 (a 15-year runway). He’s comfortable with volatility and has no plans to touch the money until then. He chooses a two-fund portfolio: 90% stocks, 10% bonds. Two ETFs. Reviews once per year.

Sam, 38, moderate FIRE timeline: Sam earns $4,800/month, invests $500/month, and is targeting FIRE at 50 (a 12-year runway). She wants international exposure and prefers a portfolio that won’t swing as sharply in bad years. She chooses a three-fund portfolio: 60% US / 20% international / 20% bonds. Reviews and rebalances once per year.

| Alex (Two-Fund, 90/10) | Sam (Three-Fund, 60/20/20) | |

|---|---|---|

| Monthly contribution | $600 | $500 |

| Expected real return (approximate) | ~6.8% (stock-heavy) | ~5.5% (more balanced) |

| Projected portfolio in 15 years | ~$196,000 | ~$131,000 |

| Worst single-year drop (historical estimate) | ~35–40% | ~25–30% |

| Maintenance per year | ~10 minutes | ~20 minutes |

Alex’s higher stock allocation gives him a higher projected outcome, but also larger potential drawdowns. Sam’s more balanced approach accepts a lower projected return in exchange for a smoother ride. Neither is the “right” portfolio in the abstract. Both are right for the person who chose them and can hold through the inevitable bad years.

To see how your own contribution amount and timeline translate into a FIRE number, run the numbers: FIRE Calculator: Estimate Your FIRE Number & Years Until Financial Independence

How to Actually Build Your Portfolio (Step by Step)

Step 1: Choose Your Allocation

Start with your FIRE timeline. If you’re more than 15 years from your target, a stock-heavy allocation (80–100% stocks) is a common starting point. Between 5 and 15 years: a mix such as 70/30 or 60/40 stocks/bonds is often more appropriate. Within 5 years of FIRE: most financial planners recommend shifting toward a more conservative allocation to protect what you’ve built.

If you haven’t calculated your FIRE timeline yet, do that first: FIRE Calculator

A second input: your actual risk tolerance. Not the theoretical one you describe in questionnaires, but the real one. During the 2020 market crash, the S&P 500 dropped about 34% in five weeks. Would you have held? Added more? Or sold? Your honest answer shapes your allocation more than any formula.

Step 2: Choose Your Funds

You don’t need to memorise specific tickers. You need to know what you’re looking for:

- Low expense ratio: under 0.20%, ideally under 0.10%. Many broad-market index ETFs charge 0.03–0.07%.

- Broad diversification: hundreds or thousands of holdings, not a narrow sector bet.

- Reputable provider: established fund companies with long track records and high assets under management.

For US investors, most major online brokerages (Fidelity, Vanguard, Schwab) offer their own low-cost index funds that meet all three criteria. Check what’s available within your specific account before choosing.

One note on ETF types: accumulating ETFs automatically reinvest dividends back into the fund, so your returns compound without any manual action. Distributing ETFs pay dividends out as cash, which you’d need to reinvest yourself. For long-term wealth building, accumulating is the simpler choice.

Step 3: Set Up Automatic Contributions

The same principle that applies to saving applies to investing: automate it on payday, before you have a chance to spend it. A fixed monthly transfer into your investment account, scheduled and forgotten, is worth more than any timing strategy over the long run.

If you haven’t built that savings automation yet: How to Save More Money: 3 Simple Tips to Improve Your Spending Habits

Step 4: Rebalance Once a Year

Rebalancing is the one piece of ongoing maintenance your portfolio actually needs. Here’s what it means and why it matters.

Over time, the assets in your portfolio grow at different rates. Say you started at 80% stocks, 20% bonds. After a strong year for stocks, you might find yourself at 87% stocks, 13% bonds, drifted away from your original plan. Rebalancing means selling a little of what grew (stocks) and buying a little of what didn’t (bonds) to bring the ratio back to 80/20.

Why does this matter? Because your target allocation exists for a reason: it reflects the level of risk that’s appropriate for your timeline and temperament. If you let the portfolio drift, you may end up taking on more risk than you intended, or less.

How to rebalance: you have two options. The first is to sell some of the overweight asset and buy more of the underweight one. This works best inside tax-advantaged accounts (like a 401(k) or IRA) where there’s no tax event. The second, often simpler for accounts where selling has tax implications, is to redirect new contributions toward the underweight asset until the ratio is restored. No selling required.

How often: once per year is enough for most investors. Some rebalance whenever an asset class drifts more than 5% from its target. Both approaches are sensible. The key is picking one and sticking to it. Not checking and rebalancing every month.

Common Portfolio Questions

Does my allocation need to change as I get closer to FIRE?

Yes, gradually. As your FIRE date approaches, you’re moving from the accumulation phase (building the portfolio) to the distribution phase (living from it). That shift carries a specific risk called sequence-of-returns risk: if markets crash in the first few years of your retirement while you’re withdrawing, the damage to your portfolio is much harder to recover from than the same crash 20 years earlier.

The standard response is to shift your allocation progressively toward bonds as you close in on your FIRE date, typically starting around 5–7 years out. This doesn’t mean abandoning stocks. Even in retirement, a long investment horizon means you still want meaningful stock exposure. A portfolio of 60% stocks and 40% bonds at FIRE is a common starting point for the distribution phase, then adjusted from there.

Your FIRE strategy also affects this. Barista FIRE or Coast FIRE investors, who plan to supplement the portfolio with some income, can often afford to keep a more aggressive allocation longer because they’re not drawing as heavily from the portfolio each year.

Should I invest in individual stocks?

For a FIRE portfolio, the answer is almost always no, at least not as the core of your strategy. The evidence is consistent: most individual investors who pick stocks underperform a simple index fund over long periods, even when they’re highly informed and disciplined. The index fund wins not because it’s smarter, but because it’s cheaper, more diversified, and immune to the behavioural mistakes that hurt individual stock pickers.

If you’re curious about the psychology behind those mistakes, The Psychology of Money [AFFILIATE LINK — ADD: The Psychology of Money] by Morgan Housel is one of the most readable explorations of how human behaviour interacts with long-term investing.

A small allocation to individual stocks (5% or less of your total portfolio, money you would be fine losing entirely) is not catastrophic if it satisfies the urge to tinker. But keep it separate from your FIRE portfolio, which should stay boring by design.

What about crypto or other alternatives?

The short answer: if you want exposure to crypto, treat it as a small speculative position, typically no more than 5 to 10% of your total portfolio for those who understand and accept the risk, and keep your core FIRE portfolio in broad-market index funds.

Crypto and alternative assets can be highly volatile, uncorrelated to traditional markets, and difficult to value. That’s both the appeal and the risk. As a supplement to a solid core portfolio, they’re a personal decision. As a replacement for that core, they create a very different and much more uncertain path to financial independence.

A dedicated guide to alternative investments and how they fit within a FIRE strategy is coming to FreedomFireHub. For now: build the foundation first.

Recommended Reading

If you want to go deeper on portfolio construction and the evidence behind long-term investing, these books are among the most useful in the FIRE and personal finance space:

- The Bogleheads’ Guide to Investing (Taylor Larimore, Mel Lindauer, Michael LeBoeuf): the practical DIY investor’s handbook. Covers asset allocation, fund selection, tax efficiency, and long-term behaviour in clear, no-nonsense terms. If you want one book that covers everything in this article in greater depth, this is it.

- Just Keep Buying (Nick Maggiulli): a data-driven case for consistent, automated investing. Maggiulli systematically addresses every reason investors try to time the market and why it almost always backfires. Highly readable.

- All About Asset Allocation (Rick Ferri): the deepest treatment of asset allocation on this list. Ferri covers the research behind different asset mixes, what the data says about international diversification, and how to build a portfolio for the long haul. A step up from the basics.

As an Amazon Associate, I earn from qualifying purchases, at no additional cost to you.

FAQ

How many funds do I actually need in a portfolio?

Fewer than you think. One fund is a complete portfolio. Two or three gives you more control over your allocation. Beyond three, the complexity tends to increase without adding meaningful diversification benefits. The most common mistake is holding ten funds that all track the same market. You haven’t diversified; you’ve just multiplied your paperwork. Start simple. Add only if there’s a clear reason to.

What’s a good stock/bond split for a 35-year-old pursuing FIRE?

With 20-plus years to a typical FIRE target, many 35-year-olds in the FIRE community lean toward 80–100% stocks. The historical evidence supports aggressive stock allocations at long time horizons, as the portfolio has time to recover from downturns. If significant volatility would cause you to sell or abandon your plan, shift toward 70/30 or 60/40 for the psychological stability. Staying invested at a slightly lower return beats panic-selling at a higher expected return every time.

How do I know if my portfolio is “too risky”?

Ask yourself one practical question: if your portfolio dropped 40% tomorrow and stayed down for 18 months, would you hold and keep contributing? If yes, your current allocation is probably fine. If that scenario would cause you to sell, reduce your stock allocation until the answer changes. Your portfolio’s job is to grow over decades, which means it needs to be something you’ll hold through the bad years, not just the good ones.

Can I build a portfolio with just $1,000?

Absolutely. Many brokerages have no account minimums, and broad-market ETFs can be bought for the price of a single share, often under $100. A $1,000 portfolio with the right structure and automatic contributions is a better starting point than a perfectly planned $20,000 portfolio that hasn’t been opened yet. The structure matters far less than starting. You can fine-tune as the balance grows.

What’s the difference between rebalancing and just buying more?

They can achieve the same outcome, but through different mechanics. Buying more means adding new money to the underweight asset until your target allocation is restored, no selling required, which makes it cleaner from a tax perspective in non-tax-advantaged accounts. Rebalancing (selling the overweight, buying the underweight) is faster and more precise, and works best inside tax-advantaged accounts where selling doesn’t trigger a taxable event. Most long-term investors use a combination: redirect contributions first, sell and rebalance only if the drift is large enough to warrant it.

Key Takeaways

- A portfolio is the sum of all your investments. One fund is a legitimate starting point. Complexity isn’t the goal, staying invested is.

- Asset allocation (how you divide your money between stocks and bonds) is the single most important portfolio decision. Match it to your timeline and your real ability to hold through downturns.

- Three simple models cover most FIRE investors: one-fund (maximum simplicity), two-fund (you control the stock/bond split), three-fund (adds international exposure). All three work.

- Rebalance once per year to keep your allocation in line with your plan. Use new contributions to rebalance where possible; sell and buy inside tax-advantaged accounts where needed.

- As you approach your FIRE date, shift gradually toward a more conservative allocation to reduce sequence-of-returns risk. Start that shift 5–7 years out, not the day before.

- Keep your FIRE portfolio boring. A simple, low-cost, diversified portfolio maintained consistently over decades outperforms complex, actively managed approaches the vast majority of the time.

Your Next Step

If you haven’t started investing yet, that comes first:

How to Start Investing for Beginners: A Simple Guide to Your First Investment

If you’re ready to see how your portfolio contributions translate into a FIRE number and timeline:

FIRE Calculator: Estimate Your FIRE Number & Years Until Financial Independence

And if you want to understand which FIRE strategy fits your situation before locking in your allocation:

The 4 Types of FIRE (Lean, Coast, Barista, Fat) Explained (With Simple Examples)

This content is for informational purposes only and does not constitute financial advice. Do your own research (DYOR) and consider speaking with a qualified professional before making any financial decisions.