Imagine two people who both want financial independence. One dreams of a simple life in a small town: mornings free, no commute, low expenses. The other wants the same freedom but with international travel, a comfortable home, and the flexibility to help family. They both want their time back. But the path that works for one would feel like a cage to the other.

That’s why the FIRE movement isn’t one destination. It’s a set of strategies with different trade-offs, and choosing the right one depends on how much you want to spend, how much you want to work, and what “freedom” actually looks like in your life.

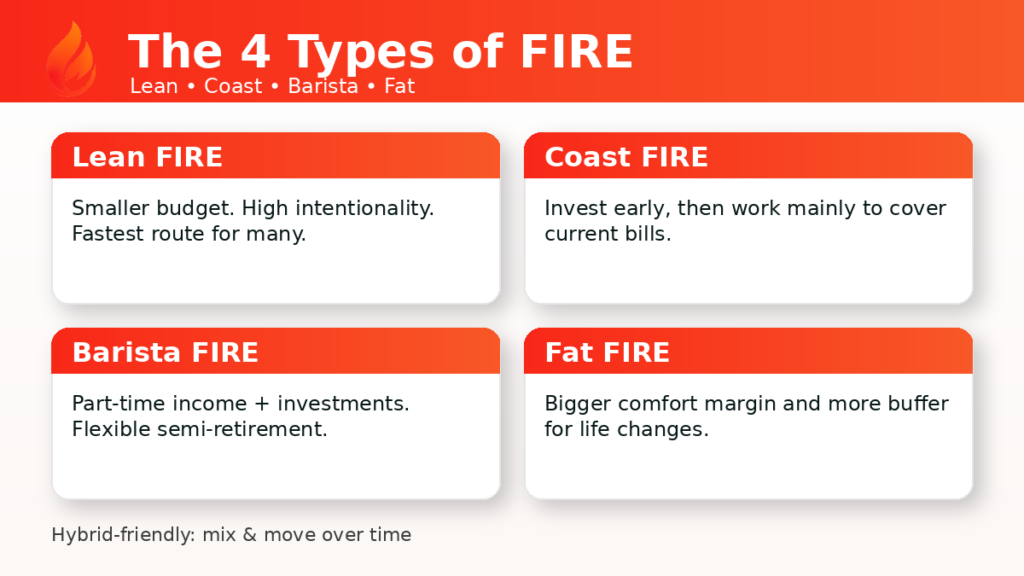

This guide breaks down the four main types of FIRE: Lean, Coast, Barista, and Fat. For each one, you’ll find a plain-English explanation, who it typically fits, realistic examples with actual numbers, and the trade-offs involved, so you can identify the approach that matches your values and situation, not someone else’s highlight reel.

Note: These types are not rigid categories. They’re labels for different trade-offs. In practice, many people build a hybrid, mixing elements over time based on what actually fits.

Quick definition: What does “FIRE” actually mean?

Financial Independence (FI) means your investments and assets can cover your living expenses. Retire Early (RE) means you have the option to stop full-time work earlier than traditional retirement age. The key word is option. Some people who reach FI still work, just on their own terms. For a deeper overview, see the full guide:

What is the FIRE Movement? Complete Guide 2026

The math behind every FIRE type is the same core formula: your annual expenses × 25 gives you a rough FIRE number, the portfolio size needed to sustain withdrawals at around 4% per year. What changes between the types is the spending level you’re targeting, and how much (if any) work you plan to do after reaching your number.

The 4 types of FIRE (at a glance)

Here’s a quick comparison to help you see the trade-offs before diving into the details.

| Type | Core Idea | Lifestyle | Work After FI? | Approx. FIRE Number* | Best For |

|---|---|---|---|---|---|

| Lean FIRE | Retire on a smaller budget | Minimalist / intentional | Usually no | $450k–$600k | People who value simplicity and low spending |

| Coast FIRE | Invest early, then coast | Comfortable, lower pressure | Yes (cover bills) | Varies by age | People who want balance and less pressure now |

| Barista FIRE | Semi-retire with part-time work | Flexible, part-time | Yes (part-time) | $375k–$625k | People who want freedom + some structure |

| Fat FIRE | Retire with a bigger budget | Higher comfort / luxury | Usually no | $1.25M–$2.5M+ | High earners who want more margin |

*Approximate ranges based on annual expenses × 25. Your actual number depends on your spending, location, and assumptions. Use the FIRE calculator below to estimate yours.

FIRE Calculator: Estimate Your FIRE Number & Years Until Financial Independence

Hybrid FIRE: You don’t have to pick just one

Before diving into each type, it’s worth knowing that many people don’t follow a single FIRE path from start to finish. Life changes, goals shift, and the most practical plans often borrow from multiple approaches.

Common hybrid paths include:

- Lean now, comfortable later: live simply in the early years to build momentum, then gradually increase spending as the portfolio grows.

- Coast + Barista: invest aggressively for a few years to reach the Coast FIRE threshold, then work part-time to cover current expenses while investments compound.

- Barista as a bridge: use part-time work for a defined period while investments mature toward full financial independence.

- “Fat-ish” FIRE: target a comfortable lifestyle with a safety margin, without pursuing the highest possible spending level.

The FIRE types below are best understood as reference points on a spectrum, not fixed destinations. The goal is to identify which trade-offs match your life, then adjust as circumstances change.

1) Lean FIRE: Financial Independence on a Smaller Budget

What Lean FIRE means

Lean FIRE is reaching financial independence with relatively low annual spending, typically in the range of $18,000 to $24,000 per year (or the local equivalent). The focus is on cutting expenses intentionally, avoiding lifestyle creep, and building a life where “enough” feels genuinely enough.

Using the ×25 formula, that spending range translates to a FIRE number of roughly $450,000 to $600,000. That’s a significantly smaller target than Fat FIRE, which is why Lean FIRE often has the shortest timeline, but also the least margin for error.

Who Lean FIRE fits well

- People who naturally enjoy a simpler lifestyle

- Those who don’t feel pressured to “keep up” with external spending norms

- Anyone willing to optimise the big categories: housing, transport, food

Common challenges

- Less cushion for emergencies, inflation, or major life changes (healthcare costs, family needs)

- A long retirement horizon (potentially 50+ years) increases exposure to sequence-of-returns risk

- Social pressure and lifestyle expectations can make sustained low spending harder than the math suggests

Lean FIRE in numbers (example scenario)

Someone spends $20,000 per year living intentionally: smaller home or shared housing, low car usage or public transport, affordable hobbies (hiking, reading, cooking at home), and conscious travel choices.

FIRE number: $20,000 × 25 = $500,000

What this means: once their portfolio reaches roughly $500,000, a 4% annual withdrawal ($20,000) could cover their expenses, and work becomes optional.

The upside is a smaller, faster target. The trade-off is less margin: there’s not much room for spending to increase without affecting the plan.

A spending tracker can help clarify whether your current lifestyle aligns with Lean FIRE numbers, or whether a different path might be more realistic. Download our free budget tracker to start mapping your expenses, or read the full guide on how to track your spending.

2) Coast FIRE: Invest Early, Then Reduce the Pressure

Most FIRE types focus on a specific spending level. Coast FIRE is different: it focuses on a specific moment in time: the point where you’ve invested enough that your portfolio can grow on its own (through compound returns) to reach a traditional retirement number by a target age, without any further contributions.

In plain language: you “buy your future retirement” early, then only need to earn enough to cover today’s bills.

Why Coast FIRE is popular

Coast FIRE is one of the most accessible FIRE strategies for beginners, because it reduces ongoing pressure. Once the Coast number is reached, you can take a lower-stress job, work fewer hours, move to a cheaper area, or take a career break, without feeling like you’ve “ruined” your long-term plan.

Coast FIRE is freedom now, not only freedom later.

Coast FIRE in numbers (example scenario)

A 30-year-old wants to have a portfolio of roughly $750,000 by age 60 (enough to cover $30,000/year in retirement using the ×25 rule). Assuming a long-term real return of around 5–6% per year, they would need approximately $130,000–$175,000 invested by age 30 to let compounding do the rest, with no additional contributions.

What this means: after reaching that threshold, they switch to a job that covers current expenses and nothing more. Their retirement plan is already on track. The key variable is time: the earlier you start, the less you need to have invested.

The Coast FIRE number depends heavily on your age, assumed return rate, and target retirement age. A FIRE calculator can help you model different scenarios.

FIRE Calculator: Estimate Your FIRE Number & Years Until Financial Independence

Common considerations

- Coast FIRE doesn’t mean you’re “done”; you still need earned income for current expenses.

- The strategy relies on long time horizons and assumed market returns, which are not guaranteed.

- Many people in Coast FIRE still invest a little, just with far less pressure.

3) Barista FIRE: Part-Time Work + Investments = Semi-Retirement

What if you didn’t need a full-time job, but didn’t want to stop working entirely either?

That’s the Barista FIRE premise. Your investments cover a portion of your expenses, and a part-time or flexible job covers the rest. The name comes from the idea of taking a simpler job (like being a barista) for supplemental income, routine, social connection, and sometimes employer benefits (depending on location).

Barista FIRE in numbers (example scenario)

Someone’s annual expenses are $30,000. Their part-time job brings in $15,000 per year. That means their investments only need to cover the remaining $15,000.

FIRE number: $15,000 × 25 = $375,000

What this means: instead of needing $750,000 for full FIRE at $30,000/year, part-time income cuts the required portfolio nearly in half. The trade-off is that earned income remains part of the equation.

If expenses are higher (say $40,000 per year with $15,000 from part-time work) the FIRE number rises to $625,000 ($25,000 × 25).

Who Barista FIRE fits well

- People who don’t want to stop working completely; they want to reduce hours, not eliminate them

- Anyone who values a safety net against market downturns (earned income acts as a buffer)

- People who want structure and social connection alongside financial freedom

Common challenges

- Part-time work isn’t always easy to find, and pay may be lower than expected

- Benefits and healthcare access vary significantly by location and employer

- You’re not fully financially independent; some dependency on earned income remains

For people who want the security of a partial income while still gaining significant freedom, Barista FIRE is often a practical middle ground, especially as a bridge to full FI.

4) Fat FIRE: Financial Independence with a Bigger Lifestyle

A common misconception first

Fat FIRE is often described as “FIRE for rich people.” That’s misleading. Fat FIRE is about spending level, not income level. The distinction matters: someone earning a high salary but spending all of it isn’t on the Fat FIRE path. Someone with a moderate income and a high savings rate over many years could be.

Fat FIRE simply means targeting a higher annual spending level in retirement, which requires a larger portfolio.

Fat FIRE in numbers (example scenario)

A couple wants a retirement lifestyle that includes travel, a comfortable home, and the flexibility to help family: roughly $50,000 to $100,000 per year in spending.

FIRE number: $50,000 × 25 = $1,250,000 (lower end)

FIRE number: $100,000 × 25 = $2,500,000 (higher end)

What this means: the larger spending target requires a substantially bigger portfolio. The timeline is typically longer, but the result includes more margin for volatility, healthcare changes, family needs, and lifestyle flexibility.

Who Fat FIRE fits well

- High earners who can save a significant amount without deprivation

- People with expensive non-negotiables (private school, frequent travel, larger home, caregiving responsibilities)

- Those who want a bigger safety margin to weather market downturns without adjusting their lifestyle

Common challenges

- Requires higher income and/or a longer accumulation period

- Lifestyle creep can turn the finish line into a moving target; if spending grows as income grows, the FIRE number keeps rising

- Taxes, property costs, and large-ticket goals matter more at higher spending levels

If you want to understand how lifestyle creep affects the timeline, the FIRE calculator can show how even small changes in monthly spending shift the numbers significantly.

FIRE Calculator: Estimate Your FIRE Number & Years Until Financial Independence

How to choose the right FIRE type for you

Step 1: Decide what “freedom” means in your life

The most useful starting point isn’t a spreadsheet; it’s a question. Ask yourself:

- Do I want to stop working entirely, or just reduce hours and pressure?

- Do I want more time now (Coast/Barista), or am I willing to wait for full independence later?

- What parts of my lifestyle are non-negotiable, and which ones could I change without losing quality of life?

The answers point toward a FIRE type more naturally than any calculator can.

Step 2: Pick your “comfort vs. speed” balance

- Lean FIRE = faster finish line, more frugal lifestyle, less margin

- Fat FIRE = slower finish line, bigger lifestyle margin, more resilience

- Coast / Barista FIRE = middle routes that trade full early retirement for flexibility and lower pressure now

Step 3: Run a simple reality check

You don’t need perfect math to start. You need direction:

- What’s your rough yearly spending? (If you’re not sure, tracking for even a few weeks reveals a lot.)

- How stable is your income?

- Do you expect major changes ahead (children, moving, home purchase, career shift)?

Once you have a rough spending number, multiply it by 25. That’s your starting FIRE target. Then test what happens when you adjust: lower expenses, higher contributions, different timelines, different FIRE styles.

FIRE Calculator: Estimate Your FIRE Number & Years Until Financial Independence

A spending tracker can help if you’re still building clarity on your real monthly costs. Download our free budget tracker to get started, or check out the full guide on how to track your spending.

Common misconceptions (that trip up beginners)

“Lean FIRE means being cheap forever”

Not necessarily. Many people on the Lean FIRE path spend intentionally on what matters and cut what doesn’t. The goal is a life where “enough” genuinely feels like enough, not a life of deprivation.

“Coast FIRE means you’re done investing”

Coast FIRE means you could stop adding new contributions and still reach your target through compounding. Many people in Coast FIRE still invest a small amount; they just do it with far less pressure and urgency.

“Barista FIRE is a step down”

If your time improves, your stress drops, and your health gets better, that’s not a downgrade. Barista FIRE is a deliberate choice to reclaim time while maintaining financial stability, and for many people, that trade-off is one of the smartest moves available.

“Fat FIRE is only for millionaires”

Fat FIRE is about a higher spending level, not a specific income threshold. The portfolio requirement is larger because the annual withdrawal is larger. Whether that’s achievable depends on savings rate, timeline, and returns, not on having a millionaire’s salary from day one.

Which type fits? Three practical scenarios

Scenario A: The “time-first” person

Values free mornings, simple routines, slow travel, and low stress. Doesn’t care about status spending. Willing to live in a smaller space and cook most meals at home.

→ Often fits Lean FIRE or Barista FIRE. The smaller target is reachable faster. If the timeline feels too aggressive, adding part-time work (Barista) provides a bridge.

Scenario B: The “balance now” person

Wants to enjoy life today, not defer everything for 15–20 years. Still wants long-term security, but isn’t willing to sacrifice the present entirely for the future.

→ Often fits Coast FIRE. Investing aggressively for a defined period, then shifting to lower-pressure work, gives this person both current quality of life and long-term trajectory.

Scenario C: The “comfort + margin” family planner

Has a partner, children, or caregiving responsibilities. Wants flexibility for housing changes, education costs, and healthcare. Prioritises resilience over speed.

→ Often fits Fat FIRE (or a comfortable version of traditional FIRE with a larger safety margin). The bigger portfolio absorbs more volatility without requiring lifestyle cuts in difficult years.

Recommended reading

If you want to go deeper on the philosophy behind FIRE types and the relationship between money, time, and freedom, these books are widely referenced across the FIRE community:

- Your Money or Your Life (Vicki Robin & Joe Dominguez): the book that shaped the FIRE mindset. Covers conscious spending, the concept of “enough,” and the “crossover point” where investment income covers expenses.

- The Simple Path to Wealth (JL Collins): a straightforward guide to index-fund investing and building long-term wealth, often recommended for Coast and Fat FIRE planners.

- The Richest Man in Babylon (George S. Clason): teaches the “save 10% first” principle in simple story form. Relevant for anyone starting their FIRE journey.

Disclosure: The links above may be affiliate links, meaning the site may earn a commission at no extra cost to you.

Key takeaways

- Lean FIRE targets lower spending ($18k–$24k/year) and a smaller portfolio ($450k–$600k). It’s the fastest path, but offers the least margin for surprises. Best suited for people who genuinely prefer a simpler lifestyle.

- Coast FIRE is about investing enough early that compounding handles the rest. After reaching the Coast threshold, you only need to cover current expenses, making it one of the most flexible strategies for people who want less pressure now.

- Barista FIRE splits the load between investments and part-time income. It’s a practical middle ground that can also serve as a bridge to full financial independence.

- Fat FIRE targets higher spending ($50k–$100k+/year) and a bigger portfolio ($1.25M–$2.5M+). It takes longer but offers more resilience and lifestyle flexibility.

- Most people end up building a hybrid, and adjusting over time, because real life doesn’t fit neatly into one label. The most sustainable FIRE plan is one that makes your life better before you hit the finish line.

- Your spending level determines your FIRE number (expenses × 25). Every reduction in recurring expenses lowers the target. Every increase in savings rate shortens the timeline. A FIRE calculator makes these relationships visible.

Your Next Step

If you want to see how your spending level translates into a FIRE number and timeline, and test what happens when you adjust expenses, contributions, or FIRE style, the most useful next step is to run your numbers:

FIRE Calculator: Estimate Your FIRE Number & Years Until Financial Independence

If you’re new to the FIRE concept and want the full foundation:

What is the FIRE Movement? Complete Guide 2026

And if you want to understand how the movement got here and why these types exist:

History of the FIRE Movement: Origins and Evolution

FAQ

Can I switch FIRE types later?

Yes. Many people start with a Lean or Coast approach to build momentum, then shift toward Barista or Fat FIRE as income rises, family situations change, or spending preferences evolve. This is one reason the Hybrid FIRE concept (above) is so common in practice; few people follow a single type from start to finish.

Do I need to retire early to “do FIRE”?

No. The most valuable part of FIRE for many people is the FI (financial independence), not the RE (retire early). Reaching financial independence means work becomes optional. Many people who reach FI continue working, but they negotiate differently, take risks they otherwise couldn’t, and make career choices based on meaning rather than necessity.

Which FIRE type is the safest?

Generally, the paths with more margin tend to feel more resilient. Fat FIRE provides a larger buffer against market downturns and unexpected expenses. Barista FIRE, with its part-time income, adds a safety net that pure portfolio-withdrawal strategies don’t have. For all types, one of the biggest long-term risks is sequence-of-returns risk: poor market returns early in retirement that can permanently damage a withdrawal plan, especially over a 50+ year horizon.

History of the FIRE Movement: Origins and Evolution

What if I like my job?

Then FIRE is working in your favour. Financial independence isn’t about quitting; it’s about removing financial desperation from your work life. When you don’t depend on the next paycheck, you make better career decisions: you negotiate from strength, you take meaningful risks, and you stay because you want to, not because you have to.

How do I calculate the FIRE number for each type?

The starting formula is the same for every type: annual expenses × 25. What changes is the spending level you target. Lean FIRE uses lower expenses, Fat FIRE uses higher ones, and Barista FIRE only needs to cover the portion of expenses not covered by part-time income. The FIRE calculator lets you model all of these scenarios:

FIRE Calculator: Estimate Your FIRE Number & Years Until Financial Independence

As an Amazon Associate, I earn from qualifying purchases, at no additional cost to you.

This content is for informational purposes only and does not constitute financial advice. Do your own research (DYOR) and consider speaking with a qualified professional before making any financial decisions.