You’ve set up the automatic transfer. You’re tracking your spending. You might even have a rough sense of your FIRE number. But every time you run the timeline, the finish line still feels impossibly far away, decades out, depending on which assumptions you use.

There’s a reason for that. And it’s probably not what you think.

Most people in the early stages of FIRE spend their energy optimizing the wrong variable: the investment returns, the FIRE number itself, or the specific funds they’re holding. These matter, but they’re largely outside your control. The variable that actually determines how fast you reach financial independence (the one you can move today) is your savings rate.

Not by a little. By years. Sometimes decades.

This guide explains what your savings rate is, why it controls your timeline more than any other single number, how to calculate yours accurately, and the practical levers for moving it higher: sustainably, without burning out or gutting your quality of life.

What Is a Savings Rate (and Why Does It Matter More Than Your Income)?

Your savings rate is the percentage of your income that you set aside and put to work: in investments, retirement accounts, or any vehicle designed to grow your net worth over time. If you earn $5,000 per month after tax and invest $1,500, your savings rate is 30%.

That sounds straightforward. But the reason savings rate matters more than income is less obvious until you see the math.

A higher income does not automatically accelerate your FIRE timeline. What accelerates your timeline is the gap between what comes in and what you spend. Someone earning $120,000 and spending $110,000 is moving slower toward financial independence than someone earning $70,000 and spending $42,000. The first person has a savings rate of roughly 8%. The second has a savings rate of 40%.

Savings rate is the compression mechanism. It does two things at once: it determines how much you can invest each month, and it determines how much income your portfolio needs to replace when you stop working. Raise your savings rate, and both numbers move in your favor simultaneously.

| Monthly Take-Home | Savings Rate | Monthly Investment | Annual Expenses | FIRE Number (×25) |

|---|---|---|---|---|

| $5,000 | 10% | $500 | $54,000 | $1,350,000 |

| $5,000 | 30% | $1,500 | $42,000 | $1,050,000 |

| $5,000 | 50% | $2,500 | $30,000 | $750,000 |

Same income, three very different trajectories. The timeline difference between 10% and 50% is not a rounding error. It’s decades.

The Math That Changes Everything

How Savings Rate Controls Your Timeline (Not Returns)

Investment returns are real and important. But here’s what’s often missed: over a typical FIRE accumulation period, savings rate explains far more of the variation in timelines than investment returns do.

The reason comes down to a double compression effect that’s unique to savings rate. When you increase your savings rate, two things happen at once:

- You invest more each month, which grows your portfolio faster.

- You spend less each month, which means your portfolio needs to be smaller to replace your income.

A higher investment return only does the first thing. Savings rate does both. That’s why it’s the lever that matters most, especially in the early and middle stages of building toward financial independence.

Here’s a worked example. Marcus earns $5,000 per month after tax and is starting from zero. At 7% real annual return:

| Savings Rate | Monthly Investment | Annual Expenses | FIRE Number | Approx. Years to FIRE |

|---|---|---|---|---|

| 10% | $500 | $54,000 | $1,350,000 | ~47 years |

| 30% | $1,500 | $42,000 | $1,050,000 | ~28 years |

| 50% | $2,500 | $30,000 | $750,000 | ~17 years |

Going from 10% to 30% shaves nearly 20 years off Marcus’s timeline. Going from 30% to 50% removes another 11. These are not marginal improvements. They are life-altering differences driven by one variable.

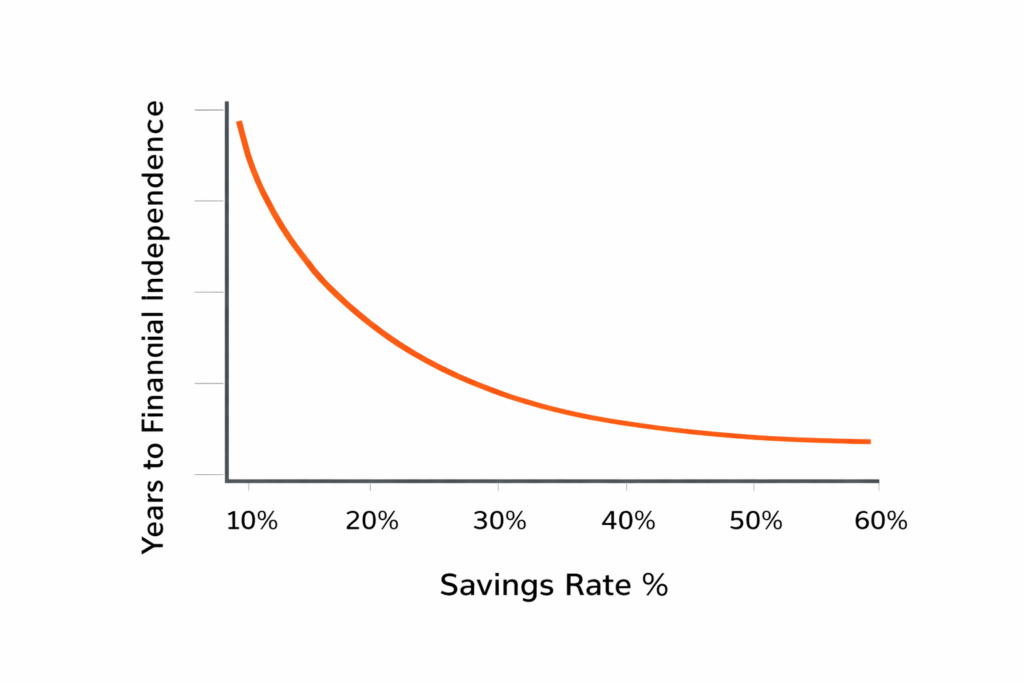

The Savings Rate to FIRE Timeline Table

The following table maps savings rate to approximate years to financial independence, assuming a 7% real annual return and starting from zero. Use it as a reference, not a precise prediction: it’s sensitive to existing savings, lifestyle changes, and actual returns.

| Savings Rate | Approx. Years to FIRE (7% real return) | Approx. Years to FIRE (5% real return) |

|---|---|---|

| 10% | ~47 years | ~54 years |

| 20% | ~37 years | ~43 years |

| 30% | ~28 years | ~33 years |

| 40% | ~22 years | ~26 years |

| 50% | ~17 years | ~20 years |

| 60% | ~12 years | ~15 years |

| 70% | ~8 years | ~10 years |

If you already have savings or investments, your timeline is shorter than this table suggests. Plug your actual numbers into the FIRE Calculator to get a personalized estimate.

How to Calculate Your Actual Savings Rate

The formula is simple:

Savings Rate = (Amount Invested or Saved ÷ Net Monthly Income) × 100

The “gross vs net” debate comes up often. Gross income includes pre-tax contributions and employer matches that never touch your bank account. Net income (take-home pay) is what you actually control. Either method works, but net income is simpler for most people and produces a more intuitive number. The key is to pick one and stay consistent: switching between them makes comparisons meaningless.

What counts toward your savings rate:

- Contributions to 401(k), IRA, or other retirement accounts (including pre-tax contributions from your paycheck)

- Employer match contributions (these are real money going to your future)

- Transfers to a taxable investment or brokerage account

- Extra debt payments above minimums on high-interest debt (you’re building net worth by reducing liabilities)

What does not count:

- Emergency fund contributions once you’ve already hit your target (topping up a fund that’s full is not investing)

- Sinking funds for known upcoming expenses (a vacation fund, a car repair fund): this is deferred spending, not savings

- Cash sitting idle in a savings account with no long-term purpose

A Worked Example

Priya earns $4,800 per month after tax. She invests $1,200 per month: $600 into her Roth IRA and $600 into a taxable brokerage account. Her savings rate is 25% ($1,200 ÷ $4,800).

At a 7% real return and starting from zero, that 25% savings rate puts her FIRE timeline at roughly 32 years.

Now Priya raises her savings rate to 35% by reducing discretionary spending and redirecting the difference to her brokerage account. Her monthly investment goes to $1,680. Her FIRE timeline drops to approximately 25 years, a reduction of 7 years from one intentional shift.

To model your own numbers and see what different savings rates do to your timeline, use the FIRE Calculator.

What Is a “Good” Savings Rate for FIRE?

There’s no universal answer, but there are useful benchmarks:

- 10–15%: The traditional retirement planning recommendation. Sufficient for a standard retirement in your mid-to-late 60s. Not enough for early retirement in most scenarios.

- 20–30%: Meaningful FIRE progress. Financial independence becomes achievable in 25–35 years depending on investment returns and starting point.

- 40–50%: The FIRE sweet spot for most people. Timelines compress to 15–22 years, making early retirement realistic without requiring extreme austerity.

- 50%+: Aggressive FIRE. Sub-15-year timelines are possible. Typically requires either a high income, very low expenses, or both.

The right savings rate is not the highest number on this list. It’s the highest rate you can maintain without burning out or consistently resenting the process. A 45% savings rate you hold for 20 years beats a 65% rate you abandon after two.

For specific strategies to raise your rate without gutting your quality of life, see How to Save More Money.

The Two Ways to Raise Your Savings Rate

Reduce Expenses: Control the Denominator

Spending less reduces your monthly outgoings, which does two things: it frees up money to invest, and it reduces the annual expenses your portfolio needs to replace. Both effects compress your timeline.

The highest-leverage expense categories are housing, transportation, and food. These three typically account for 60–70% of most households’ spending. Small percentage reductions here produce larger savings than eliminating dozens of smaller line items.

The silent killer of savings rate is lifestyle inflation: the gradual upward drift of spending that tends to match income growth, leaving the gap unchanged even as you earn more. Every raise absorbed into lifestyle is a raise that did nothing for your FIRE timeline.

The most practical first step is an honest picture of where your money actually goes. Download the free Budget Tracker to map your current spending, or read How to Track Your Spending for a step-by-step approach to building that picture from scratch.

Increase Income: Expand the Numerator

Every dollar of extra income that you don’t spend improves your savings rate directly. The key word is “don’t spend”: income growth only moves the needle when it widens the gap rather than funding a higher lifestyle baseline.

For most people in stable employment, salary negotiation is the highest-ROI income move available: one conversation, no extra hours, permanent result. For detail on how to approach that conversation and what to do when the answer is no, see How to Negotiate a Raise or Promotion. For a broader view of income growth strategies beyond your primary job, How to Increase Your Income covers freelancing, side hustles, and the sequencing that tends to work best for people in the FIRE accumulation phase.

The Combination Effect

The real leverage comes when both levers move at once. Sofia earns $5,500 per month and is currently saving 22%, investing $1,210 per month. She negotiates a $5,000 annual raise ($417/month after tax) and cuts $300/month from discretionary spending by cancelling unused subscriptions and reducing food delivery.

Total change: +$717/month to her savings. Her savings rate jumps from 22% to approximately 35%. Her FIRE timeline drops by roughly 8 years. Neither change required a dramatic lifestyle overhaul: one was a single conversation, the other was a deliberate spending review.

Your Savings Rate and the Different FIRE Styles

The savings rate you need depends on which version of FIRE you’re pursuing. The four main FIRE styles each have different implications for how hard you need to push this lever.

Lean FIRE requires the highest savings rate sustained over time, because your target is a small portfolio covering minimal expenses. The math works in your favor (small FIRE number) but demands long-term discipline on spending.

Coast FIRE requires an aggressive savings rate in the early years, then almost nothing afterward. The strategy is to invest enough early that compound growth carries you to your FIRE number without additional contributions. Once you’ve “coasted,” the pressure on savings rate drops dramatically.

Barista FIRE is a middle path. Accumulate enough to cover most expenses from your portfolio, then use part-time work to cover the remainder. This reduces both the required savings rate and the total FIRE number, at the cost of not being fully work-free.

Fat FIRE requires a longer accumulation period because the target portfolio is large, but it doesn’t require extreme frugality. Higher income can compensate for a more moderate savings rate. The timeline is longer, but the lifestyle during accumulation is less restricted.

None of these paths is inherently better. The right one is the one that fits your income, your expenses, and what you actually want your post-FIRE life to look like.

Common Savings Rate Mistakes

Switching between gross and net income. Calculating one month on gross and the next on net makes your savings rate look inconsistent when it isn’t. Pick one baseline and stick with it.

Counting sinking funds and emergency buffer top-ups as savings. Money earmarked for a vacation, a car repair, or Christmas gifts is deferred spending. It’s worth tracking, but it doesn’t belong in your savings rate calculation.

Confusing saving with investing. Cash sitting in a savings account earning 0.5% is not working for your FIRE number. Undeployed cash held indefinitely is losing purchasing power to inflation. Savings rate counts money that is actually invested and growing.

Optimizing for the number rather than the habit. A savings rate of 55% that you maintain by white-knuckling every purchase eventually breaks. The burnout rebound, when it comes, tends to be expensive. A sustainable rate you can hold for 15–20 years is worth more than a heroic rate you abandon in year three.

Not revisiting your rate as income grows. If your income has increased and your savings rate hasn’t, lifestyle inflation has captured the difference. Review your rate every six months and after every significant income change.

Recommended Reading

These books offer three distinct angles on the savings rate mindset and the math behind it:

- Your Money or Your Life (Vicki Robin & Joe Dominguez): The book that shaped how the FIRE movement thinks about savings rate at a philosophical level. Robin reframes money as “life energy” (hours of your life exchanged for income) which changes how you evaluate every spending decision. The history of the FIRE movement traces directly back to this book’s influence. For readers who want the mindset beneath the math, this is the place to start.

- Just Keep Buying (Nick Maggiulli): A data-driven examination of the savings and investing decisions that actually move the needle. Maggiulli covers when to save more versus when to invest more, how to think about savings rate in different income situations, and why consistency beats optimization. Grounded in evidence, readable, and directly relevant to the accumulation phase of FIRE.

- The Simple Path to Wealth (JL Collins): The bridge between savings rate and investing. Collins argues that the savings rate is the single most important variable in building wealth, and then explains exactly what to do with the money once you’ve saved it. If you’ve read the investing guide and want to go deeper, this is the clearest next step.

As an Amazon Associate, I earn from qualifying purchases, at no additional cost to you.

FAQ

What’s the difference between savings rate and investment return: which matters more?

In the early and middle stages of FIRE accumulation, savings rate matters more for most people. Investment returns compound over time, but they’re largely outside your control. Savings rate is something you can change this month. The exception is late-stage accumulation, when a large portfolio means that return differences have a bigger absolute impact. Early on, prioritize the rate.

Should I calculate my savings rate on gross or net income?

Either works. Net income (take-home pay) is simpler for most people and produces a more intuitive number. Gross income includes pre-tax contributions that may never touch your bank account, which can make the calculation feel detached from your actual cash flow. Pick one method and apply it consistently. Switching between them produces meaningless comparisons.

Does my employer’s 401(k) match count toward my savings rate?

Yes. Employer match contributions are real money going into your investment account. Including them gives you a more accurate picture of your total savings rate. If you’re not capturing the full match, you’re leaving compensation on the table: that free money should be the first thing you prioritize before any other savings optimization.

What if I have high debt: should I focus on debt payoff or savings rate?

iHigh-interest debt (above roughly 7% APR) is effectively a guaranteed negative return on your net worth. Paying it down aggressively improves your financial position just as reliably as investing. The exception: always contribute enough to your 401(k) to capture the full employer match, even while paying down debt. Beyond that, direct extra money at high-interest debt first. For the full framework, see How to Pay Off Debt.

Is a 50% savings rate realistic on an average income?

For some people, yes. It depends on fixed costs more than income. In a high cost-of-living area with dependents, 50% may be genuinely out of reach on an average income without significant lifestyle changes. In a lower cost-of-living area, or with shared housing costs, it’s more achievable. The goal is not to hit a specific number but to understand where you are and move the rate incrementally higher. Even moving from 15% to 25% changes your timeline significantly.

How often should I recalculate my savings rate?

Review it every six months and after any significant income or expense change: a raise, a new recurring cost, a change in housing. Your savings rate is not a one-time calculation; it’s a metric that should evolve with your situation. Tracking it quarterly gives you early warning when lifestyle inflation is quietly capturing income gains before they reach your investment account.

Key Takeaways

- Your savings rate is the percentage of your income that you invest or save toward net worth growth. It’s the single variable with the most leverage over your FIRE timeline.

- Savings rate compresses your timeline from both sides at once: it increases what you invest and reduces what your portfolio needs to replace. No other variable does this.

- Calculate it as: (Amount Invested ÷ Net Monthly Income) × 100. Include employer matches and extra debt payments. Exclude sinking funds and emergency buffer top-ups.

- 10–15% is traditional retirement territory. 40–50% is the FIRE sweet spot. The right number is the highest rate you can sustain without burning out.

- The two levers are expenses (spending less lowers your FIRE number and frees up cash) and income (earning more expands what’s available to invest, as long as lifestyle stays controlled).

- Review your rate every six months. Lifestyle inflation is silent: if income rises but your savings rate stays flat, the gain has been captured by spending, not by your future.

Your Next Step

Calculate your current savings rate using this month’s numbers: amount invested divided by take-home pay, times 100. Then open the FIRE Calculator and see what your timeline looks like, and what happens to it if you raise your rate by 5% or 10%.

FIRE Calculator: Estimate Your FIRE Number & Years Until Financial Independence

If you need a clearer picture of your current spending before you can calculate accurately:

How to Track Your Spending (Step-by-Step)

And if you want specific strategies to raise your rate without overhauling your life:

How to Save More Money: 3 Simple Tips to Improve Your Spending Habits

This content is for informational purposes only and does not constitute financial advice. Do your own research (DYOR) and consider speaking with a qualified professional before making any financial decisions.